B2B Payment & Credit Management: A Comprehensive Playbook for Indian SMEs

Turning Pending into Paid Made for Indian MSMEs

B2B commerce runs on trust—trust that goods will arrive and invoices will be paid. But delayed payments, credit risks, and operational bottlenecks can choke that trust and your cash flow. This playbook offers a 360‑degree look at B2B payment and credit management, blending policy, process, and technology so your SME stays liquid while scaling sales.

1. The Credit‑to‑Cash Cycle Explained

Credit Assessment → Vet customer using financials, bureau score, trade references.

Credit Limit Setting → Assign safe exposure based on five‑pillar model.

Order Approval → Auto‑check against limit before processing.

Invoicing → Generate e‑invoice, attach PO, deliver promptly.

Payment Collection → Reminders, dunning, multiple channels.

Cash Application → Match payments to invoices, reconcile.

Analytics & Review → Ageing, DSO, limit adjustments.

Digital platforms like PayAssured connect these stages into one workflow.

2. Building a Robust Credit Policy

Risk Categories — A (score ≥ 80), B (60‑79), C (40‑59), D (< 40).

Terms Matrix — A: Net 45, unsecured; B: Net 30, BG optional; C: 50 % advance; D: CBD.

Approval Levels — Sales ≤ ₹5 L can approve limits up to 50 % of policy; finance head approves higher.

Review Frequency — Quarterly for A/B, monthly for C/D.

3. Modern Payment Methods & Best Fits

| Method | Speed | Cost | Best For |

| NEFT/RTGS | Same‑day | Low | High‑value domestic payments |

| UPI B2B | Instant | Nil to low | Small recurring orders |

| Cards/QR | Instant | 1‑2 % fee | E‑commerce or one‑off buys |

| LC/SBLC | Bank‑guaranteed | Moderate fees | Large, high‑risk deals |

| Escrow | Release on milestones | Moderate | Projects with multiple deliverables |

4. Automating Collections

Dunning Ladder — Friendly reminder (D‑3), Reminder 2 (D+7), Final notice (D+30).

Multi‑Channel — Email + WhatsApp + phone.

Smart Links — UPI QR, Razorpay hosted page inside reminder.

Interest Auto‑Calc — MSME Act; add to invoice after 45 days.

Platforms like PayAssured trigger auto‑holds and calculate interest seamlessly.

5. Risk Mitigation Tools

| Tool | What It Does | When to Use |

| Trade‑Credit Insurance | Covers up to 90 % of invoice default | High‑value buyers, export deals |

| Invoice Discounting/TReDS | Get cash early, bank takes payment risk | Smooth seasonal cash gaps |

| Bank Guarantee | Buyer’s bank promises payment | New buyer, large capex order |

| Retention of Title Clause | Ownership until full payment | Goods with resale value |

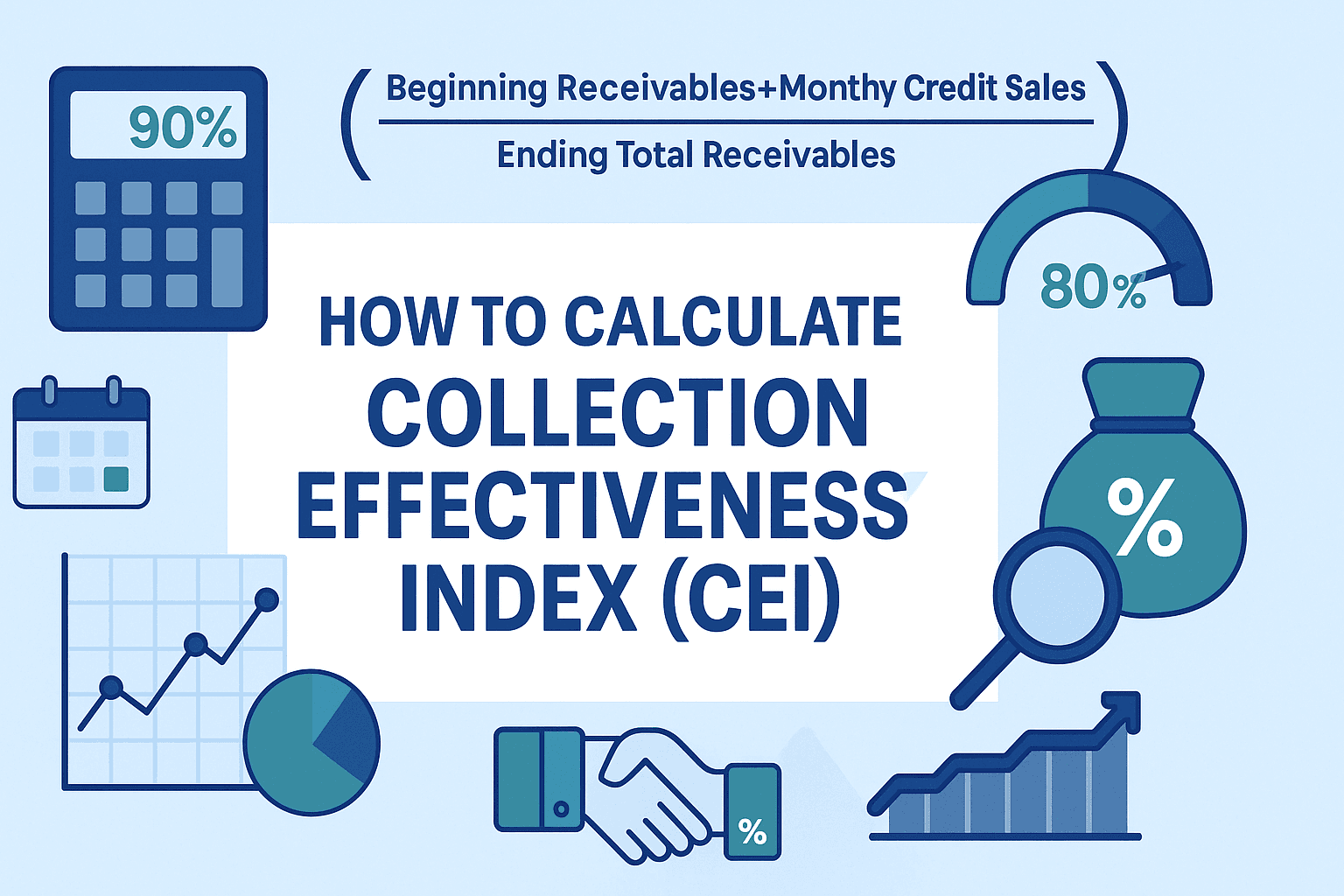

6. Key KPIs to Track

| KPI | Target |

| DSO | < 45 days |

| % 90+ Day Bucket | < 5 % of total AR |

| Bad‑Debt Ratio | < 0.5 % of sales |

| Average Payment Delay | < 10 days |

| Collector Effectiveness | \> 80 % |

Visualise these on dashboards; review in weekly finance huddles.

7. Legal & Compliance Essentials

MSME Act Sec 15‑18 — 45‑day limit, 3× RBI interest.

GST 180‑Day Rule — Leverage ITC reversal threats.

Sec 138 Cheque Bounce — Criminal remedy for dishonoured cheques.

Arbitration Clause — Fast dispute resolution seat in your city.

8. Technology Stack Checklist

Cloud ERP (Tally Prime, Zoho Books) — Core accounting.

PayAssured — Credit scoring, reminders, insurance linking.

Payment Gateway (Razorpay, Cashfree) — UPI/card links.

BI Tool (Google Looker Studio) — Real‑time KPI dashboards.

9. Common Pitfalls to Avoid

Extending limit without updated financials.

Mixing personal and business collections.

Ignoring small delays—they snowball.

Lack of cross‑department alignment (sales vs finance).

10. Action Plan for the Next 30 Days

Draft/Update credit policy; share with sales.

Onboard to PayAssured for ageing dashboard.

Automate D‑3 and D+7 reminders with payment links.

Pull bureau reports for top 20 buyers; adjust limits.

Train team on MSME interest calculation and legal notices.

Remember: Great products drive sales; great credit management turns sales into cash.