Accounts Receivable Insurance Guide: Protect Your Cash Flow Against Customer Defaults

Turning Pending into Paid Made for Indian MSMEs

Unpaid invoices can choke a business. Accounts Receivable (AR) Insurance—often called trade‑credit insurance—shields you from that risk by paying up to 90 % of your receivable if a buyer fails to pay. This guide explains how AR insurance works, who needs it, and how to choose the right policy in India.

1. What Is Accounts Receivable Insurance?

A policy that compensates your business when a customer defaults due to insolvency, protracted slow payment, or political risk (for exports).

Covers domestic and export sales.

Premiums usually range 0.15 %–0.75 % of insured turnover, depending on buyer quality and sector.

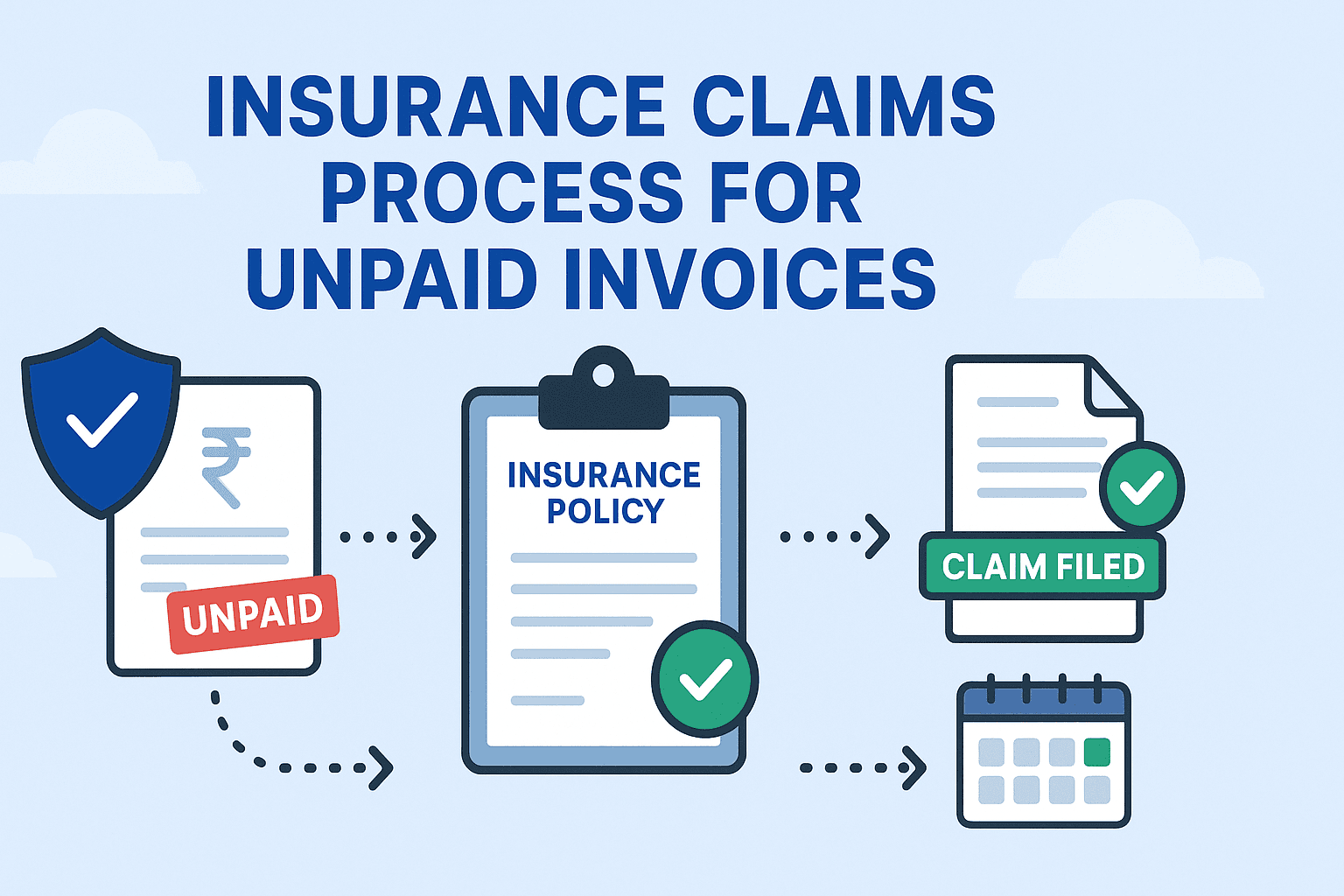

2. How It Works in Five Steps

Credit Assessment – Insurer scores each buyer and sets a credit limit.

Selling on Credit – You ship goods/services within that approved limit.

Monitoring – Insurer (or platform like PayAssured) alerts you to rating downgrades.

Claim Trigger – File a claim if payment is overdue beyond the waiting period (typically 90 days) or buyer files for bankruptcy.

Indemnity Payment – Insurer pays the insured percentage (usually 90 %) minus deductible.

3. Benefits for SMEs

| Benefit | Why It Matters |

| Protects Cash Flow | Default compensation keeps operations running |

| Bank Financing | Banks discount insured invoices at better rates |

| Sales Growth | Safely extend credit to new or higher‑risk buyers |

| Market Intelligence | Free credit reports and alerts bundled in |

4. Policy Types

| Policy Type | Best For | Notes |

| Whole Turnover | Businesses with diverse customer base | Cheapest rate; all receivables covered |

| Named Buyer | Firms with a few large buyers | Higher rate per rupee, but focused cover |

| Single Invoice/Shipment | One‑off high‑value deals | Short‑term cover; useful for exports |

5. Key Policy Parameters to Review

Coverage Percentage – Typically 80 – 90 % of invoice.

Deductible / First Loss – Amount you absorb before insurer pays.

Maximum Liability – Cap per buyer and per year.

Waiting Period – Days after due date before you can claim.

Exclusions – Disputes, force majeure, or contrived delays.

6. Claim Checklist

Copies of invoice, purchase order, and delivery proof.

Reminder emails and formal demand letters.

Statement of account showing overdue status.

Proof of buyer insolvency filing (if applicable).

Submit within policy‑defined timeframe—late filing can void coverage.

7. Choosing the Right Insurer or Broker

Credit Rating – Insurer rated A‑ or better by ICRA/CRISIL.

Platform Tools – Dashboard, API integration, auto‑limit updates (PayAssured integration is a plus).

Claims Support – Dedicated team, track record of prompt settlements.

Sector Fit – Experience in your industry reduces premium.

8. Common Mistakes to Avoid

Forgetting to declare new buyers or limit breaches.

Waiting too long to notify overdue invoices.

Insuring exports only, leaving domestic receivables exposed.

9. Integrating AR Insurance with Your Credit Policy

Use as a safety net, not a crutch—still vet buyers.

Bundle with invoice discounting—banks lend more against insured AR.

Automate compliance—PayAssured can flag limit breaches and late notifications.

10. Key Takeaways

AR insurance transfers customer‑default risk to an insurer, protecting cash flow.

Premiums are modest relative to the hit from even one major default.

Choose policy structure (whole turnover, named buyer, single invoice) to match customer mix.

Pair with robust credit management for maximum protection.

Remember: Selling on credit shouldn’t feel like gambling. Insure your receivables and grow with confidence.