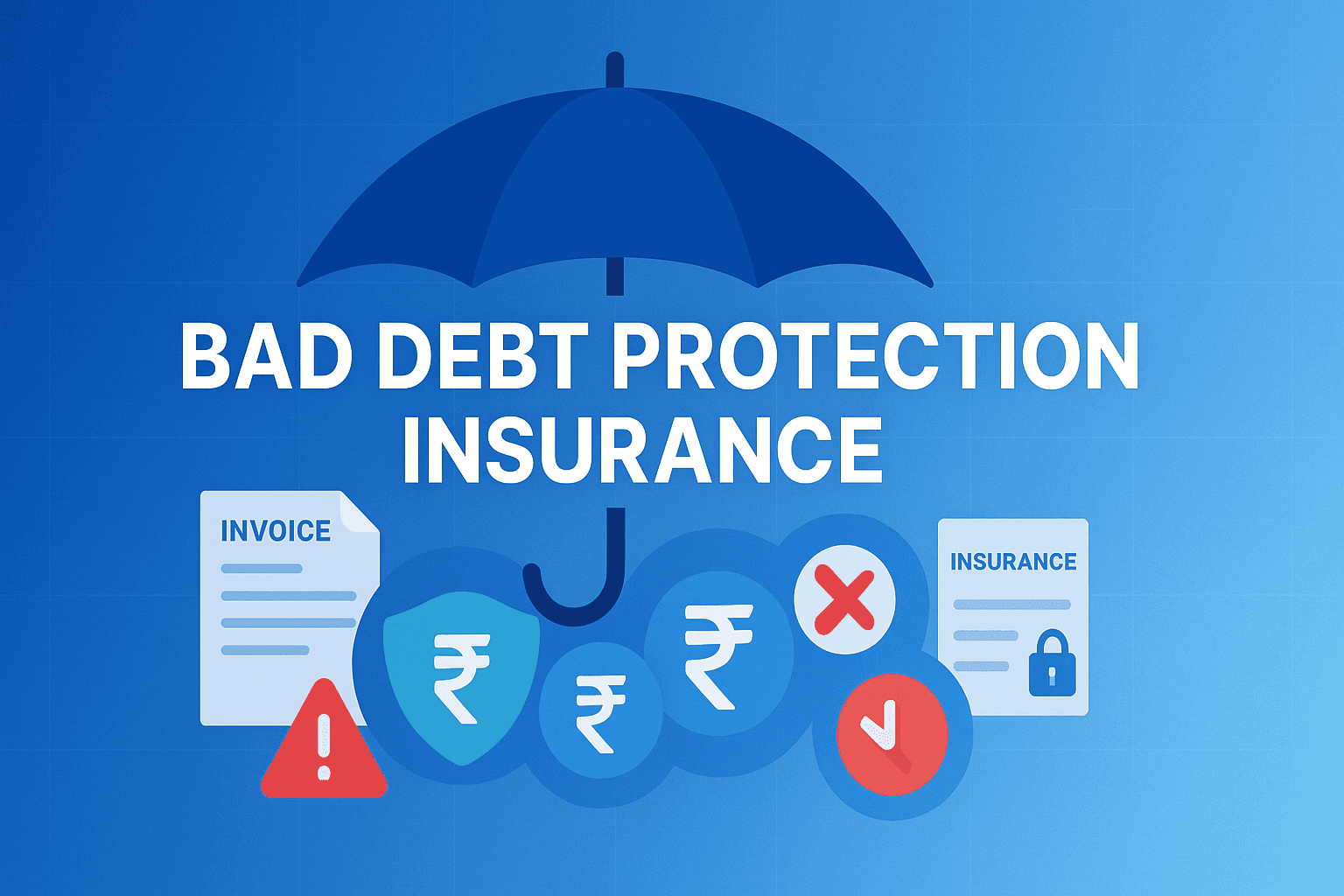

Bad Debt Protection Insurance: Safeguarding Your Receivables

Turning Pending into Paid Made for Indian MSMEs

When a customer defaults, the loss slices straight into profit. Bad Debt Protection Insurance—also called trade‑credit insurance—transfers that risk to an insurer, letting you sell on credit with confidence. This guide explains how the cover works, why Indian SMEs should care, and the practical steps to get protected.

1. What Exactly Is Bad Debt Protection Insurance?

A policy that pays up to 90 % of the invoice value if a buyer fails to pay due to insolvency, protracted default, or political risk (for exports).

Covers both domestic and export sales; some insurers offer hybrid policies.

Premiums are usually 0.15 %–0.75 % of annual insured turnover—lower for well‑rated portfolios.

2. How It Works in Practice

Credit assessment. Insurer (or a platform like PayAssured) scores each buyer and assigns an exposure limit.

Sales on credit. You ship goods / deliver services as usual within the approved limit.

Monitoring. Insurer sends alerts on rating downgrades; you can adjust exposure to stay covered.

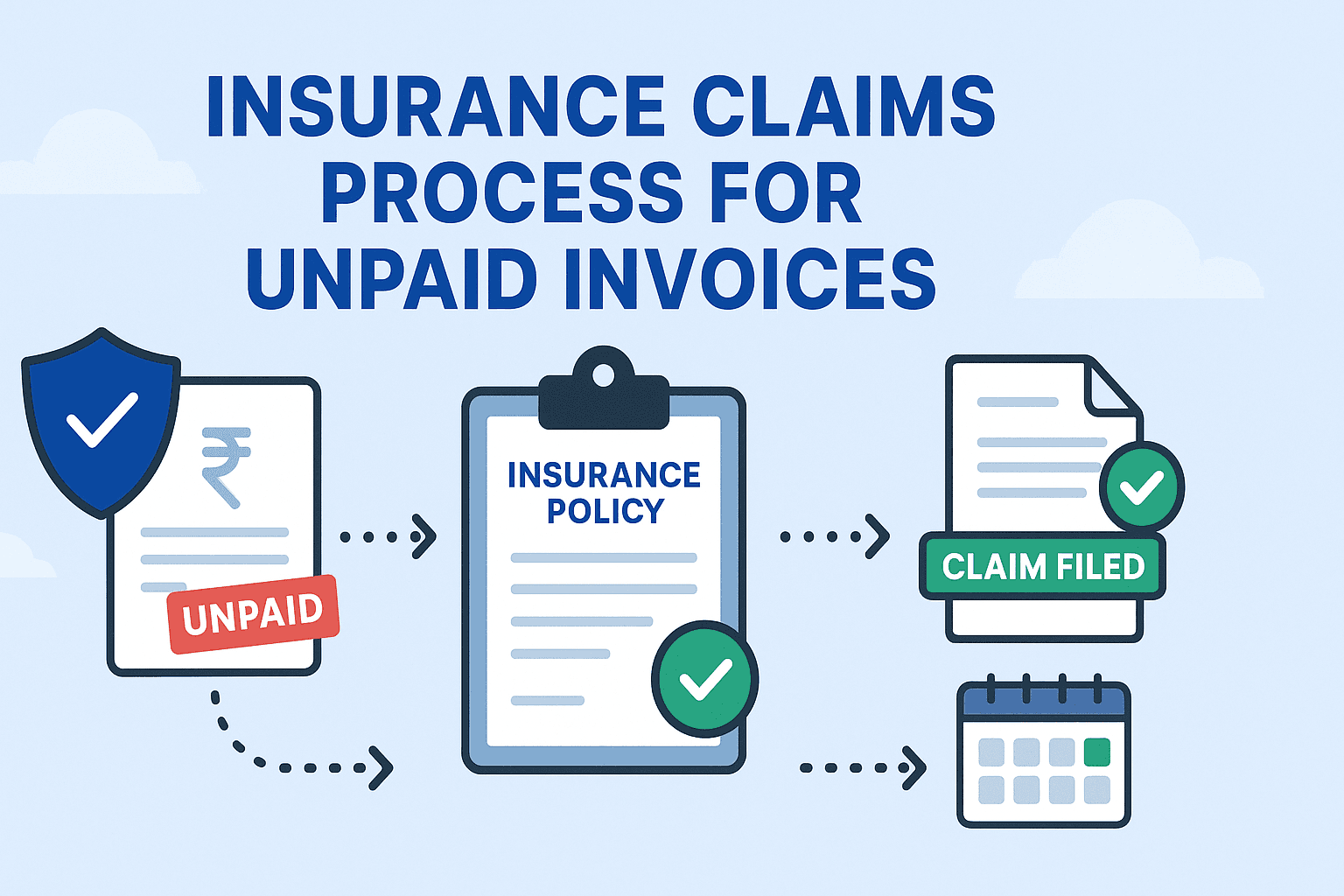

Claim trigger. If buyer doesn’t pay within waiting period (e.g., 90 days after due date) or files insolvency, you file a claim.

Payout. Insurer pays the insured percentage (say, 90 %), minus deductible, usually within 60 days.

3. Key Benefits for SMEs

Cash‑flow stability. Recover most of the sale value even if the buyer collapses.

Better bank terms. Banks discount insured receivables at higher advance rates and lower interest.

Sales growth. Confidently extend higher limits or longer terms to win new clients.

Risk insight. Free credit reports and continuous monitoring come bundled with many policies.

4. Factors Affecting Premiums

| Factor | Impact |

| Buyer quality (CIBIL/Experian score) | Higher scores → lower premium |

| Industry risk (steel vs. pharma) | High‑risk sectors cost more |

| Average credit period | Longer terms increase risk and premium |

| Claims history | Clean record reduces rates |

| Policy structure (whole‑turnover vs. select buyers) | Cherry‑picking costs more per rupee insured |

5. Policy Structures

Whole Turnover: All eligible domestic sales insured; lower admin, cheaper rate.

Named Buyer: High‑value customers only; useful if a few accounts dominate revenue.

Single Invoice / Single Shipment: One‑off cover for big export orders.

6. Claim Process Cheat‑Sheet

Notify insurer within 30 days of due‑date breach.

File supporting docs: invoice, PO, POD, SOA, reminder emails.

Cooperate in debt‑collection efforts; recoveries above excess are shared back.

Receive payout after waiting period; continue to pursue recovery if required.

7. Choosing the Right Insurer or Platform

Insurer rating: Look for A‑ or higher (ICRA/CRISIL).

Sector expertise: Some specialise in agri, others in engineering.

Digital tools: Dashboards, API integration, automated credit‑limit updates (see PayAssured).

Service quality: Dedicated claim‑handling team matters when things go wrong.

8. Common Mistakes to Avoid

Forgetting to declare new buyers or limit breaches—voids coverage.

Waiting too long to notify overdue accounts.

Insuring only exports while large domestic receivables remain exposed.

9. Key Takeaways

Bad Debt Protection Insurance turns uncertain receivables into bankable assets.

Premiums are modest compared to the cost of one major default.

Choose a policy structure that matches your customer mix and risk appetite.

Pair insurance with disciplined credit management for bulletproof cash flow.

Remember: Growth is good—but only when backed by protection. Cover your receivables before they cover your balance sheet in red.